Futures Market: Overnight, LME copper opened at $9,678.5/mt, dipping to a low of $9,664/mt shortly after the opening bell. It then edged higher before pulling back and fluctuating rangebound. Towards the close, it surged to a high of $9,719.5/mt, eventually closing at $9,695/mt, up 0.49%. Trading volume reached 13,000 lots, while open interest stood at 268,000 lots. Overnight, the most-traded SHFE copper 2507 contract opened at 78,640 yuan/mt, fluctuating rangebound in the early session to a low of 78,470 yuan/mt. It then fluctuated upward throughout the session, reaching a high of 78,730 yuan/mt near the close. The contract closed slightly lower at 78,650 yuan/mt, up 0.45%. Trading volume reached 20,000 lots, while open interest stood at 189,000 lots.

[SMM Copper Morning Meeting Summary] News: (1) On June 13 (Friday), Condor Resources announced that its Cobreorco copper project in the Andahuaylas province of central Peru had passed a "significant" permitting milestone after its environmental impact statement was approved, bringing the project closer to the drilling phase. The permitting process was carried out by Teck Resources, which entered the project through an option and joint venture agreement with Condor at the end of 2023.

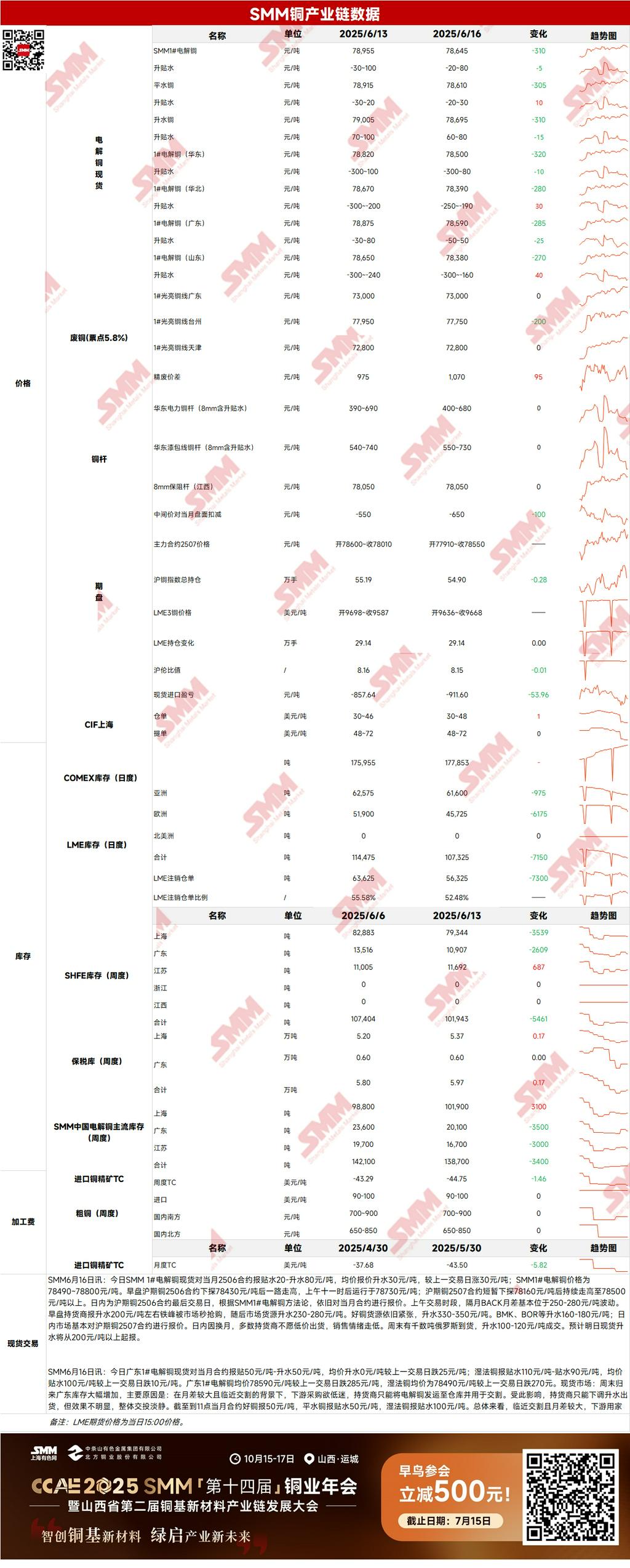

Spot: (1) Shanghai: On June 16, SMM #1 copper cathode spot prices were quoted at a discount of 20 yuan/mt to a premium of 80 yuan/mt against the front-month 2506 contract, with an average premium of 30 yuan/mt, up 30 yuan/mt from the previous trading day. SMM #1 copper cathode prices ranged from 78,490 to 78,800 yuan/mt. In the morning session, the SHFE copper 2506 contract dipped to 78,430 yuan/mt before rising steadily, trading around 78,730 yuan/mt after 11 a.m. The SHFE copper 2507 contract briefly dipped to 78,160 yuan/mt before continuing to rise above 78,500 yuan/mt. As June 16 was the last trading day for the SHFE copper 2506 contract, quotes were still made against the front-month contract in accordance with SMM #1 copper cathode methodology. During the morning trading session, the BACK price spread between futures contracts fluctuated mainly within the 250-280 yuan/mt range. Due to contract rollover, most suppliers were reluctant to sell at low prices, and selling sentiment weakened. Several thousand tons of Russian copper arrived over the weekend, with transactions concluded at premiums of 100-120 yuan/mt. Spot premiums are expected to start above 200 yuan/mt tomorrow.

(2) Guangdong: On June 16, Guangdong #1 copper cathode spot prices were quoted at a discount of 50 yuan/mt to a premium of 50 yuan/mt against the front-month contract, with an average premium of 0 yuan/mt, down 25 yuan/mt from the previous trading day. SX-EW copper was quoted at a discount of 110 yuan/mt to a discount of 90 yuan/mt, with an average discount of 100 yuan/mt, down 10 yuan/mt from the previous trading day. The average price of Guangdong #1 copper cathode was 78,590 yuan/mt, down 285 yuan/mt from the previous trading day, while the average price of SX-EW copper was 78,490 yuan/mt, down 270 yuan/mt from the previous trading day. Overall, as the delivery date approaches and the price spread between futures contracts is relatively large, downstream consumers are adopting a wait-and-see attitude, resulting in generally light trading activity.

(3) Imported copper: On June 16, warrant prices ranged from $30 to $48/mt, with QP in June, and the average price increased by $1/mt compared to the previous trading day. B/L prices ranged from $48 to $72/mt, with QP in July, and the average price remained unchanged from the previous trading day. EQ copper (CIF B/L) prices ranged from $4 to $18/mt, with QP in July, and the average price remained unchanged from the previous trading day. Quotations were based on cargo arrivals expected in late June and early July. Overall, the intentions of buyers and sellers are gradually converging, and activity is expected to recover after June [date].

(4) Secondary copper: On June 16, the price of secondary copper raw materials remained unchanged MoM. The price of bare bright copper in Guangdong ranged from 72,900 to 73,100 yuan/mt, unchanged from the previous trading day. The price difference between copper cathode and copper scrap was 1,070 yuan/mt, increasing by 95 yuan/mt MoM. The price difference between copper cathode rod and secondary copper rod was 1,190 yuan/mt. According to an SMM survey, secondary copper rod enterprises reported that copper prices have risen, and the price increase of secondary copper raw materials is in line with that of copper cathode. However, compared to the quotation stage for secondary copper raw materials at noon last Friday, there was no significant difference. Therefore, today's quotations from secondary copper rod enterprises remained unchanged from last Friday. Moreover, the current procurement objective of secondary copper rod enterprises is solely to meet immediate daily production needs. Even if there are pending delivery orders on hand, they are not in a hurry to procure sufficient secondary copper raw materials.

(5) Inventory: On June 16, LME copper cathode inventory decreased by 7,150 mt to 107,325 mt. On the same day, SHFE warrant inventory increased by 10,782 mt to 47,051 mt.

Price: On the macro front, despite the escalating conflict between Israel and Iran, the US dollar has not demonstrated strong safe-haven characteristics. Meanwhile, the Bank of England, Swiss National Bank, Riksbank, and Norges Bank will all announce their interest rate decisions, and the US dollar index still has some downside room, which is bullish for copper prices. On the fundamental front, yesterday, due to contract rollover, the selling sentiment of most suppliers declined, and they were unwilling to sell at low prices. There were significant differences in copper cathode prices among various brands during the day, with large fluctuations in premiums for different brands. High-quality copper was in short supply, and some brands had higher premiums. As of Monday, June 16, SMM's nationwide copper inventories in major regions increased by 2,900 mt WoW to 147,700 mt, marking the third consecutive Monday of inventory buildup. Compared to the inventory changes from last Thursday, inventories in most regions across the country increased. On the price front, it is difficult for macro and fundamental factors to form a resonance, and it is expected that there will be limited upside room for copper prices today.

[The information provided is for reference only. This article does not constitute direct advice for investment research and decision-making. Clients should make cautious decisions and should not rely on this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.]